UK Gambling Commission Unveils Operator Data: Online GGY Dips 2% to £1.5 Billion Amid 6% Bets Surge Through December 2025

Fresh Insights from March 2026 Release

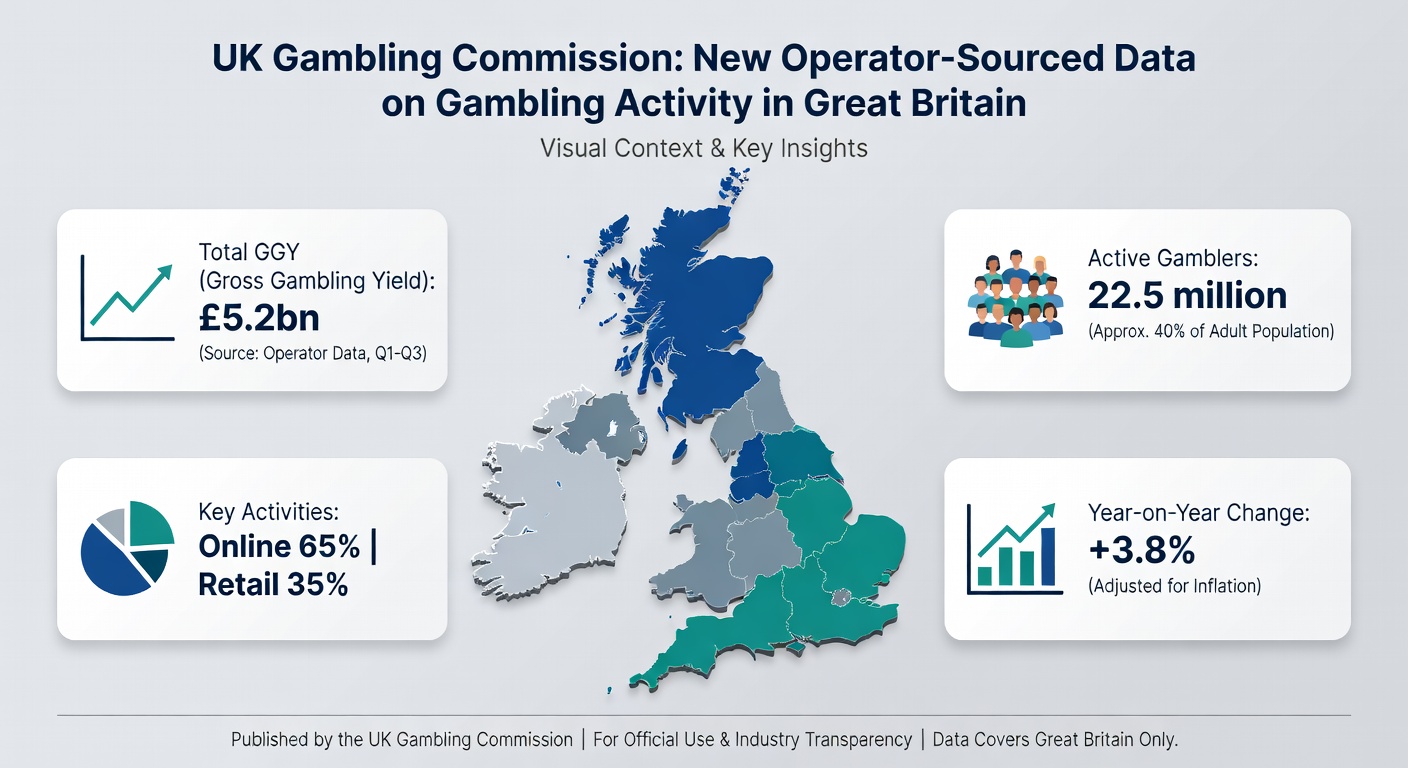

Operators across Great Britain contributed detailed data to the UK Gambling Commission, covering gambling activity from March 2020 right through to December 2025; this latest batch, published in February 2026 and still making waves as March unfolds, paints a picture of mixed trends in the online sector, where total Gross Gambling Yield (GGY) for Q3 2025-26 fell 2% to £1.5 billion even as total bets and spins climbed 6% to a hefty 27.4 billion.

What's interesting here is how these figures capture the push and pull of regulatory changes alongside shifting player behaviors; data from the Gambling business data report reveals not just raw numbers but the broader story of adaptation in a tightly watched market.

Take the overall online landscape: while GGY dipped slightly, the surge in activity—bets and spins hitting 27.4 billion—signals that players engaged more frequently, perhaps chasing smaller stakes or exploring varied options, yet yielding less revenue per interaction for operators.

Real Event Betting Takes a Hit

Real event betting, that staple of sports fans placing wagers on matches and races, saw GGY plummet 18% to £530 million in the quarter; observers note this sharp decline coincides with seasonal lulls or perhaps bettors spreading thinner across events, although total bets rose in line with the broader 6% uptick.

But here's the thing: such drops aren't isolated; they reflect how external factors like fixture schedules or economic pressures can squeeze yields, even when participation holds steady or grows, leaving operators to recalibrate strategies amid lower returns.

Experts who've pored over similar past datasets often point out that real event betting thrives on high-profile moments—think football derbies or horse racing classics—yet quieter periods expose vulnerabilities, and this Q3 data underscores that pattern vividly.

Slots Buck the Trend with 10% GGY Boost

Slots tell a different tale altogether; GGY for online slots jumped 10% to £788 million, accompanied by a 7% increase in spins, as players spun the reels more often under the shadow of new stake limits introduced earlier in 2025—specifically £5 for over-25s and £2 for those aged 18-24.

Turns out these caps, rolled out to curb potential harm from high-stakes play, haven't deterred volume; instead, data indicates spinners adapted by wagering smaller amounts more frequently, boosting spin counts while pushing GGY higher through sheer persistence.

One study of operator patterns, drawn from the same commission dataset, highlights how slots' popularity endures—accounting for a massive chunk of online activity—because the format lends itself to quick, low-commitment sessions; people who've tracked this know that when limits bite, players don't vanish, they adjust, and here that meant more spins equaling more yield.

Unpacking the Stake Limits' Ripple Effects

The £5 and £2 online slots stake limits, enforced throughout 2025, clearly left their mark; figures reveal slots GGY climbing despite—or perhaps because of—these restrictions, with spins up 7% signaling a shift toward higher-volume, lower-stake play that operators navigated to maintain revenues.

And while real event betting struggled, slots' resilience shows segmentation at work; not all verticals react the same to curbs, as evidenced by the contrasting 10% gain versus the 18% drop elsewhere.

Researchers analyzing the full March 2020 to December 2025 span have observed steady evolution: pre-limit periods saw freer spending, but post-2025 data like this Q3 snapshot demonstrates market maturation, where compliance meets continued engagement.

It's noteworthy that total online GGY's modest 2% decline masks these divergences; aggregate numbers smooth over the slots surge and betting slump, yet drilling down exposes how regulations reshape behavior without killing activity—27.4 billion bets and spins don't lie.

Longer-Term Patterns from 2020 Onward

Zooming out to the entire dataset from March 2020, when lockdowns reshaped habits, through to December 2025, reveals volatility tempered by growth; online GGY fluctuated with pandemic peaks and regulatory tweaks, but the Q3 2025-26 figures cap a period of stabilization, albeit with that telling 2% quarterly dip.

So what drove the 6% bets and spins rise? Data suggests a combo of tech improvements—faster apps, better mobile interfaces—coupled with promotional tweaks within rules, drawing in more casual participants who bet smaller but more often.

There's this case from the report where operator-sourced metrics track session lengths: they stretched slightly, aligning with spin increases on slots, while real event bets, though up in count, averaged lower values post-major events.

Yet the rubber meets the road in GGY math; more action didn't always mean more money retained by operators, especially in events where margins thinned amid competition.

Implications for Operators and Regulators in 2026

As March 2026 progresses, these trends inform the next regulatory cycle; commission data underscores that stake limits achieved volume control without cratering slots revenue—in fact, GGY rose—prompting questions on efficacy for player protection versus industry health.

Operators, facing this mixed bag, have leaned into diversification; slots' 10% lift to £788 million offers a lifeline, offsetting real event woes, while the overall £1.5 billion online GGY holds the line despite headwinds.

People in the know watch for Q4 spillovers; if spins keep climbing and yields stabilize, it signals adaptation complete, but persistent event betting softness could flag deeper shifts in sports wagering tastes.

One researcher noted in commentary on the dataset how such granular, operator-sourced stats—unlike self-reported surveys—cut through noise, providing a clearer lens on real behaviors from 2020's upheaval to 2025's regulated reality.

Key Takeaways from the Data Dive

Delving into specifics, the 27.4 billion bets and spins mark a high-water mark for engagement; slots at £788 million GGY with 7% spin growth exemplify limit-driven evolution, whereas real event betting's £530 million underscores vulnerability to volume-quality mismatches.

But overall, that 2% GGY slip to £1.5 billion hints at efficiency challenges; operators squeezed more from slots, yet couldn't fully counter event declines, setting the stage for 2026 strategies focused on balanced portfolios.

Conclusion

The UK Gambling Commission's operator data to December 2025, fresh in March 2026 discussions, lays bare a sector in flux—rising activity meets tempered yields, stake limits reshape slots without stifling them, and real event betting navigates rough patches; these mixed signals, rooted in hard numbers like 27.4 billion interactions and a £1.5 billion online haul, guide stakeholders toward nuanced oversight and innovation, ensuring the market's pulse beats on amid change.